Realised by: Meriem Dridi; Nour Houda Fajraoui; Iheb Zarraa; Alaa Dhibi

Students in:

Master’s in International Trade and Strategy

(Commerce International et Stratégies)

École Supérieure de Commerce ESCT (Manouba)

Under the direction of:

Dr Habiba Nasraoui Ben Mrad

Financial development refers to the evolution of a country’s financial institutions, markets, instruments, and the legal framework that supports them. According to the World Bank, the financial sector includes the set of institutions and rules that enable credit, savings, investment, and risk-sharing. Its fundamental objective is to reduce information, transaction, and contract enforcement costs, thereby improving the allocation of resources within the economy.

How does financial development contribute to economic growth across countries, and under what conditions does it enhance or potentially hinder long-term economic performance?

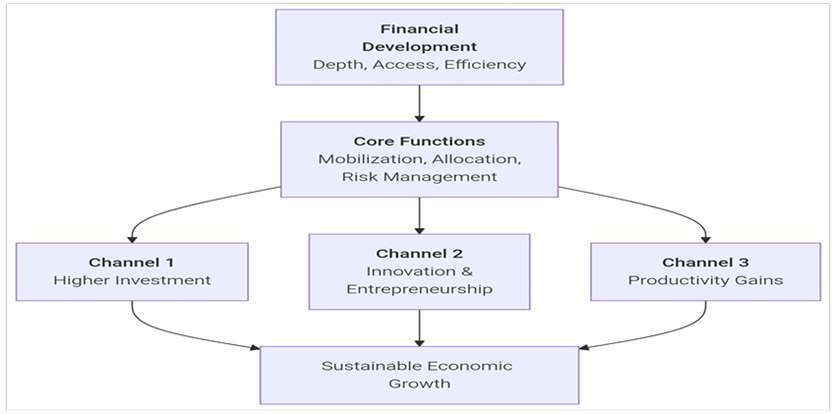

I. How Does a Financial System Transform Savings into Economic Growth ?

1. From Intermediation to a Catalyst for Growth

Both classical and modern economic theories converge on a key idea: the financial system is not merely an intermediary between savers and investors; it acts as a genuine catalyst for economic growth.

As early as the beginning of the twentieth century, Joseph Schumpeter emphasized the role of banks as “engines of development,” capable of financing innovative entrepreneurs and supporting technological progress. This intuition has been reinforced by contemporary approaches, notably those of Ross Levine, who argues that financial development enhances capital efficiency by reducing information and transaction costs.

2. The Four Essential Functions of a Financial System

A well-functioning financial system drives growth through four essential functions:

➢ It mobilizes savings by transforming numerous small individual resources into significant volumes of capital;

➢ It allocates capital efficiently by channeling funds to the most productive investments;

➢ It improves risk management through diversification and insurance mechanisms;

➢ It facilitates economic transactions by reducing payment and contracting costs.

3. How Can Financial Development Be Measured?

Précisons d’abord que les systèmes financiers diffèrent selon qu’ils soient dominés par les banques ou par les marchés des capitaux.

Empirical analysis of financial development generally relies on four key dimensions:

➢ Financial depth measures the size of the financial sector relative to the economy, using indicators such as private credit or stock market capitalization as a share of GDP;

➢ Access evaluates the proportion of households and firms with access to formal financial services;

➢ Efficiency reflects the degree of competition and intermediation costs;

➢ Stability measures the resilience to crises, namely the system’s ability to withstand shocks and financial crises.

These indicators make it possible to compare financial systems across countries and to assess their contribution to economic performance.

II. Global Results and Trends

1. When Finance Becomes Excessive

Recent research by the International Monetary Fund highlights a non-linear relationship between finance and growth. While financial deepening stimulates economic activity at low and intermediate levels of development, its marginal benefits decline beyond a certain threshold. This inverted U-shaped relationship has given rise to the concept of “too much finance.”

“Too much finance” concept:

When private credit exceeds roughly 100 percent of GDP, its positive impact on growth tends to weaken and may even turn negative. Advanced economies, where credit and debt ratios are high, face complex trade-offs between growth, financial instability, and crisis risks. By contrast, many developing countries remain in a favorable zone where financial deepening continues to act as a lever for growth and stability.

2. Key Global Indicators (World Bank / IMF)

International data confirm these patterns.

Private Credit / GDP

○ Advanced economies: often > 100% of GDP

○ Global average private-sector debt: ~143% of GDP (U.S. ~143%, China ~206%)

○ Growth benefits wane when credit/GDP becomes very high

Stock Market Capitalization / GDP

○ Global market capitalization ≈ 112% of world GDP (2024)

○ Advanced economies: stock markets often exceed GDP

○ Developing economies: much smaller market depth

Financial Inclusion

○ 79% of adults worldwide have an account (Global Findex)

○ Large gaps:

● Sub-Saharan Africa: ~55%

● North America & Western Europe: ~90%

○ Mobile banking rising sharply (84% phone ownership in low- and middle-income countries)

The rapid expansion of digital finance and mobile banking is nevertheless contributing to a gradual reduction in these gaps.

3. Global Trends and Takeaways

❖ Emerging markets are experiencing faster growth in private credit and market depth, yet still trail advanced economies.

❖ Most emerging economies remain in the “favorable zone” where more financial deepening equals more growth and stability (IMF).

❖ Mature economies shift from banking-dominated systems to capital-market-oriented finance.

III. Financial Development and Economic Growth: The Case of India

1. Context: India’s Financial Transformation

India provides a particularly illustrative example of the link between financial development and growth. Economic reforms initiated in 1991 profoundly transformed the country’s financial system through the liberalization of the banking sector, the development of capital markets, and increased openness to international financial flows. The financial sector became a core driver of India’s economic transition.

How Financial Development Supported Growth

This modernization enabled greater mobilization of savings, increased financing of infrastructure, and stronger integration of the Indian economy into global financial networks. Improved capital allocation, the rise of non-bank financial institutions, and the development of venture capital have fostered innovation and enhanced productivity in both industry and services.

2. Key Mechanisms

❖ Better capital allocation: improved risk assessment, lower intermediation costs, more competitive banking environment

❖ Growth of non-banking financial companies (NBFCs) and venture capital supporting innovation

❖ Enhanced productivity in manufacturing and services through improved access to credit

3. Empirical Outcomes and Limitations

Empirical evidence shows a positive relationship between indicators of financial development and GDP growth. However, challenges remain, including regional inequalities in access to credit, financial exclusion in rural areas, and episodes of banking fragility linked to the accumulation of non-performing loans.

4. Policy Lessons and What India Still Needs

❖ Strengthen macroprudential regulation to ensure financial stability

❖ Expand long-term financing channels for industrial upgrading

❖ Advance digital and inclusive finance while controlling credit risks

❖ Maintain reforms to support sustained and balanced growth

IV. Challenges and Risks of Uncontrolled Financial Development

1. Financial Development Is Not Without Risks

When financial growth outpaces real economic needs, it can fuel asset bubbles and financial instability, as seen in the 2008 crisis. More finance is not always better.

In countries with weak institutions, poor governance, corruption, and weak regulation can lead to inefficient lending and capital misallocation, often favoring well-connected firms rather than the most productive ones. Moreover, despite significant progress, financial exclusion remains a major challenge. Small and medium-sized enterprises, rural populations, and women are often excluded from formal financial systems, thereby limiting the potential for inclusive growth.

2. Strategic Interventions for Sustainable Finance

In this context, public policy plays a crucial role by:

➢ Strengthening regulation and supervision, particularly through macroprudential tools, to prevent financial imbalances;

➢ Promoting inclusive finance supported by digital technologies to expand access while reducing costs;

➢ Building trust through financial literacy and consumer protection to increase participation and reduce vulnerability.

3. Future Trends and Evolving Landscapes: New Frontiers in Finance

Emerging trends such as fintech, green and sustainable finance, central bank digital currencies (CBDCs), and geopolitical shifts like dedollarization are reshaping contemporary financial systems. While these developments offer substantial opportunities, they require appropriate regulatory frameworks to reconcile innovation, stability, and consumer protection.

4. Key Takeaways for Policymakers: A Balanced Path Forward

❖ Financial development must be balanced—deep yet stable, inclusive yet efficient

❖ The goal is resilient systems that support real economic activity without creating instability

❖ Smart policies can turn finance into a force for sustainable and equitable growth, especially in developing economies

Conclusion

We can conclude that finance is a means, not an end. Financial development plays a central role in supporting countries’ economic growth. A strong and efficient financial system helps mobilize savings, improve access to credit, and channel resources toward productive investments. Global evidence shows that countries with deeper and more inclusive financial systems tend to grow faster and more sustainably. However, financial development must be supported by good regulation, strong institutions, and policies that ensure stability and inclusion. Examples such as India demonstrate that well-managed financial development can stimulate innovation, support economic activity, and improve living standards. Used wisely, finance remains a vital instrument in the service of long-term economic growth.

Realised by: Meriem Dridi; Nour Houda Fajraoui; Iheb Zarraa; Alaa Dhibi